有两种纳税申报人身份可供选择。一种称为蓝表申报人,另一种称为白表申报人。如果您有自己的公司或拥有自己的个人事业,您应该选择蓝表申报人身份作为您的纳税身份,这种身份享有诸多好处,而且您基本上不会有任何损失。 将损失结转至未来的好处 蓝表申报人身份在税务方面享有诸多好处,但最大的好处是,您将被允许将税收损失结转到未来10年。举例来说,如果您今年(第1年)的税收损失为1000万日元,而您在下一年(第2年)的应税收入为1200万日元,如果您是蓝表申报人,那么您第2年的应税收入将仅为200万日元。如果您是白表申报人,您的应税收入将是1200万日元,因为您无权结转税收损失,而是需要根据每年的收入纳税。因此,如果您产生了税收损失,这种情况一旦发生,每年都会被浪费;如果您产生了应税收入,您将须就全部收入纳税。 对于个人事业主来说,还有另一项比较大的税务好处。您将可以从应税收入中额外扣除650,000日元。如果您的年收入在扣除各项费用后为5,000,000日元,那么您将适用30%的边际税率(国税税率为20%,居民税税率为10%)。https://www.nta.go.jp/taxes/shiraberu/taxanswer/shotoku/2260.htm您每年可以节省195,000日元的税款。如果您经营事业20年,您将共节省3,900,000日元的税款。这是一笔可观的数目。至少,对我来说是这样。 如何申请蓝表申报人 您应该向税务局提交以下表格。https://www.nta.go.jp/law/tsutatsu/kobetsu/hojin/010705/pdf/056-1.pdf提交成功后,您将从下一年开始成为蓝表申报人。 申请蓝表报税人的截止日期 对于新成立的公司,必须在3个月内提交申请表格。对于个人事业主,必须在2个月内完成提交。对于已经经营多年的既有公司和个人事业主,如果想申请下一年度的蓝表申报人,则必须在当前财政年度结束之前提交申请。对于想申请2023日历年度蓝表申报人的公司,必须在2022年底之前提交申请。对于想申请某一年度蓝表申报人的个人事业主,必须在该年度3月15日之前提交申请。例如,如果某个人事业主想申请2023年度蓝表申报人身份,其必须在2023年3月15日之前提交申请。

消费税出口退税时的须知事项 最近,日本政府在没有太多公告的情况下改变了出口退税的规则。对于寄送物品到外国并期望获得消费税退税的出口企业,这项改变可能有重大影响。 以下是日本国税厅发布的公告。 公告的基本内容是说,出口商品在20万日元以下时,必须通过日本邮政(JAPAN POST)的EMS或其他服务寄送。 这听起来可能有些不公平,因为现在市场上还有FEDEX、UPS和其他物流公司,而日本邮政并不一定是其中的第一名。 曾经有一位客户向我们抱怨,日本邮政提供寄送服务的国家和区域有限,他有一些顾客就不在服务范围之内。他还说,EMS不一定够快。有时候用EMS要一个星期才能寄到的商品,用FEDEX几天就寄到了。 但是规则就是规则。如果有出口企业无视了这项要求,就有风险无法获得其应得的消费税退税。 这项新规定出台的背景,可能是因为过去发生了很多骗税行为。日本政府或许认为,强制出口企业使用一个半官方机构(也就是日本邮政)进行寄送的话,会减少很多不诚实的报税行为。 https://www.nta.go.jp/publication/pamph/shohi/r03kaisei.pdf

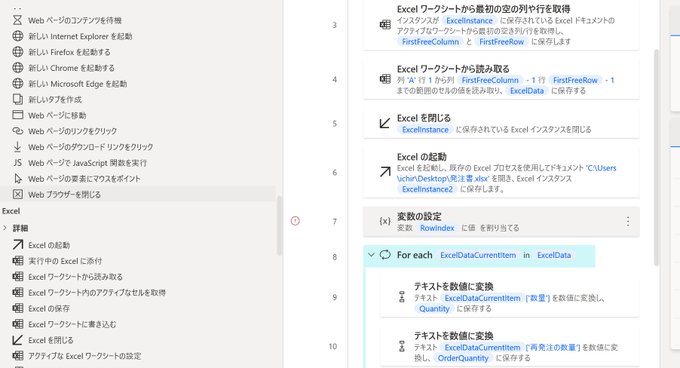

今日も中小企業の経理を効率化するツールについて、書いてます。今回もRPA(MicrosoftのPower Automate)です。 RPAとPythonの違いは、GUI(デスクトップで、目で見てデスクトップに見えているボタンなどの部品をクリックする操作法)で操作できるか出来ないかの違いです。 Pythonの方が遥かにモジュールも沢山あるし色々な事が出来るのですが、一般ユーザーから見たGUIの操作は出来ません。Pythonではこのアプリのこのボタンを押して、ファイルを開けて人間の目でどの情報を使うかを選んで、コピーして、貼り付けるなんてことは出来ません。 私の事務所で結構実現したいと思っているのが、達人と言うソフトで作った法人税と消費税の申告書データを電子申告する事なのですが、Pythonではこれは逆立ちしても出来ません。ソフトを立ち上げて、申告するお客さんの名前を選んで、電子署名を付けて、パスワードを入力して、電子申告の達人から送信する。これは全部Windowsで表示されるソフトのUIを識別する必要がありますが、RPAではボタンの外観(UI)を識別して、クリックする事が出来るので、まだやっていないのですが、もしかしたら可能でしょう。 Power Automateでは下記のように色々なアプリを使うコマンドが沢山あります。でも、Pythonのライブラリーの数に比べたら、大人と子供の喧嘩のようなもので、多分レベルが違います。 ただ、プログラミングが出来ない人でも使えるように設計されているので、普通の人でもちょっとトレーニングすれば出来るようになるかも知れません。 うちの事務所でも皆に一度デモを見せて、各々の仕事に各自がプログラムを使って応用できる所があるか、意見してもらおうと思います。実際のプログラミングは皆が覚えるより、担当者を決めてその方にやってもらう方が、全然効率的だとは思います。

事務所の業務を効率化をするために、色々ツールを触っています。 今回は、Microsoftが提供しているPower Automateというものを試してみました。Power AutomateはいわゆるRPAの一つで、デスクトップ上で動くプログラムです。 デスクトップの下の所にあるメニュー・バーのボタンを画像として認識して、それをクリックする事が出来る様なので不思議なプログラムです。 ウェブサイトはリンクやチェックボックスなどのパーツを認識しているので、HTMLのタグも読むことが出来る様です。HTML上のテーブルからデータを持ってくることも可能なようです。 今回はこの本のサンプルを使って、ウェブからデータを持ってきて、その一部を取り出す作業をやって見ました。IF文やFOR EACH文などがあり、そのデータを使って、エクセルに書き出したり、メールを出したり、コマンドプロンプトまであったりで、結構いろんな事が出来そうでした。 AzureやAWSのコマンド・メニューなどもありましたが、一体に何に使うのだろう。データベースやPDFファイルの書き出しや読み込みに関するメニューもあったので、いっぱしのプログラミング言語のようでした(失礼!)。いや本当、デスクトップの上をベースにすると言う普通ではない状況を別にすれば、普通のプログラミング言語のように使えそうです。

If you have to get a recruiting license or renew, to get a real estate agency or brokerage license, or renew, you have to have more than certain amount of net asset as its requirement. If your company has made losses in recent years, has eaten up paid-in capital and does not have enough net … Read More “To switch a loan to capital, then offset against carried loss – steps to make a company with negative net asset to net positive” »

Companies and sole proprietors doing business in Japan will be required to put its CT (Consumption Tax) Number on your invoices for your customers to claim the Consumption Tax they have paid to you against their CT liabilities. The new system will come into effect from Oct. 1, 2023. Companies and sole proprietors who want … Read More “Qualified Invoice Issuer Number 適格請求書発行事業者. The Question is whether Qualify or Better Not Qualify?” »

Tax Permanent Resident status vs Permanent Residency for VISA 税法意义上的永住者vs 签证意义上的永住者 People sometimes get confused about the concept of tax Permanent Resident with Rermanent Resident for VISA. They are separate concepts. 人们很容易混淆税法上的永住者和签证意义上的永住者。它们其实是两个不同的概念。 Being a Permanent Resident (PR) for VISA does not necessarily mean you are a Permanent Resident for tax. PR for visa is a … Read More “Tax Permanent Resident status vs Permanent Residency for VISA 税法意义上的永住者vs 签证意义上的永住者” »

This is one of the frequently asked questions. Basic rule: Non permanent tax resident is not taxable for foreign source income unless the gain is repatriated into Japan The basic rule is that foreign sourced income of non-permanent tax residents (who have been in Japan more than 5 years in the past 10 years) is … Read More “Is capital gain from foreign stocks I purchased before I came to Japan taxable or not taxable? Talking about 特定有価証券の譲渡” »

There are lots of businesses that receive orders from customers overseas and buy goods in Japan for margins. We also have several clients doing the business too. Their margins are relatively low in many cases that is mostly in the range between 1% to 10%. Some businesses only charges 300 yen per item. Still they … Read More “Trap to get a consumption tax refund when your business buys goods and export overseas 購買代行で気を付けなければいけない落とし穴” »

Recently Japanese Yen became even weaker to almost 145 yen per USD. I received a question from a client today whether exchange gain will be reportable or not for Japanese Income Tax. It would feel a bit unreasonable if one had to pay tax on the gain if her savings were accumulated even before she … Read More “Income tax on currency exchange gain” »